The following presentation materials will be used by Union Bankshares Corporation at one or more investor relations events, or meetings with analysts or existing or potential investors, during the third quarter of 2017. 1 FILED BY UNION BANKSHARES CORPORATION PURSUANT TO RULE 425 UNDER THE SECURITIES ACT OF 1933 AND DEEMED FILED PURSUANT TO RULE 14a - 12 UNDER THE SECURITIES EXCHANGE ACT OF 1934 SUBJECT COMPANY: XENITH BANKSHARES, INC. (Commission File No. 001 - 32968) Date: July 24, 2017

Investor Presentation July 2017

3 Forward Looking Statements Certain statements in this presentation may constitute “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward - looking statements are statements that include projections, predictions, expectations, o r beliefs about future events or results or otherwise are not statements of historical fact, are based on certain assumptions as of the ti me they are made, and are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified. Such state men ts are often characterized by the use of qualified words (and their derivatives) such as “expect,” “believe,” “estimate,” “plan,” “p roj ect,” “anticipate,” “intend,” “will,” “may,” “view,” “opportunity,” “potential,” or words of similar meaning or other statements co nce rning opinions or judgment of Union Bankshares Corporation (“Union” or “UBSH”) or its management about future events. Such statements include statements as to the anticipated benefits of the merger, including future financial and operating results, cost savings and e nha nced revenues as well as other statements regarding the merger. Although Union believes that its expectations with respect to forward - looking statements are based upon reasonable assumptions within the bounds of its existing knowledge of its business and oper ati ons, there can be no assurance that actual results, performance, or achievements of Union will not differ materially from any projected future results, performance, or achievements expressed or implied by such forward - looking statements. Actual future results and trends may differ materially from historical results or those anticipated depending on a variety of factors, including but not limited t o: (1) the businesses of Union and Xenith Bankshares , Inc. may not be integrated successfully or such integration may be more difficult, time - consuming or costly than expected; (2) expected revenue synergies and cost savings from the merger may not be fully realized or realized within the expected time frame; (3) revenues following the merger may be lower than expected; (4) customer and emplo yee relationships and business operations may be disrupted by the merger; (5) the ability to obtain required regulatory and share hol der approvals, and the ability to complete the merger on the expected timeframe may be more difficult, time - consuming or costly than expected; (6) changes in interest rates, general economic conditions, tax rates, legislative/regulatory changes, monetary and fi scal policies of the U.S. government, including policies of the U.S. Treasury and the Board of Governors of the Federal Reserve Sy ste m; the quality and composition of the loan and securities portfolios; demand for loan products; deposit flows; competition; demand f or financial services in the companies’ respective market areas; their implementation of new technologies; their ability to develop and ma int ain secure and reliable electronic systems; and accounting principles, policies, and guidelines, and (7) other risk factors detai led from time to time in filings made by Union with the Securities and Exchange Commission (the “SEC”). Forward - looking statements speak only as of the date they are made and Union undertakes no obligation to update or clarify these forward - looking statements, whether as a result of new information, future events or otherwise.

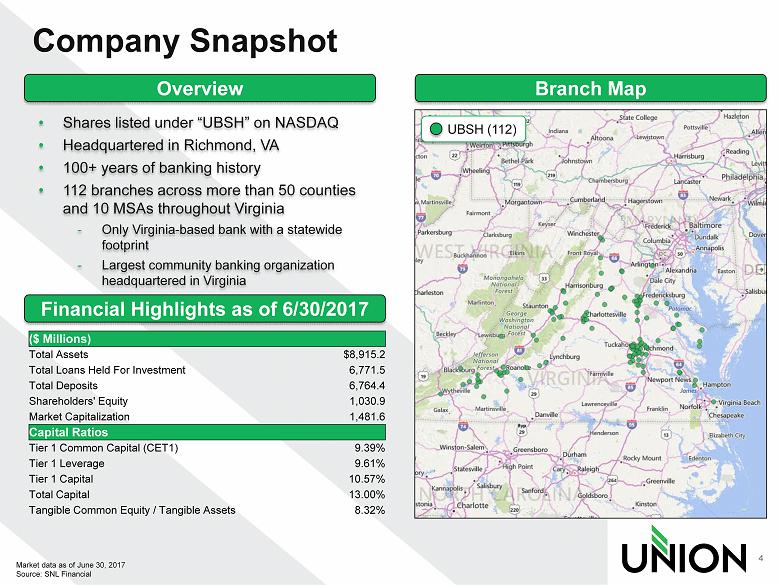

Company Snapshot 4 Overview Branch Map • Shares listed under “UBSH” on NASDAQ • Headquartered in Richmond, VA • 100+ years of banking history • 112 branches across more than 50 counties and 10 MSAs throughout Virginia - Only Virginia - based bank with a statewide footprint - Largest community banking organization headquartered in Virginia Financial Highlights as of 6/30/2017 Market data as of June 30, 2017 Source: SNL Financial UBSH (112) ($ Millions) Total Assets $8,915.2 Total Loans Held For Investment 6,771.5 Total Deposits 6,764.4 Shareholders' Equity 1,030.9 Market Capitalization 1,481.6 Capital Ratios Tier 1 Common Capital (CET1) 9.39% Tier 1 Leverage 9.61% Tier 1 Capital 10.57% Total Capital 13.00% Tangible Common Equity / Tangible Assets 8.32%

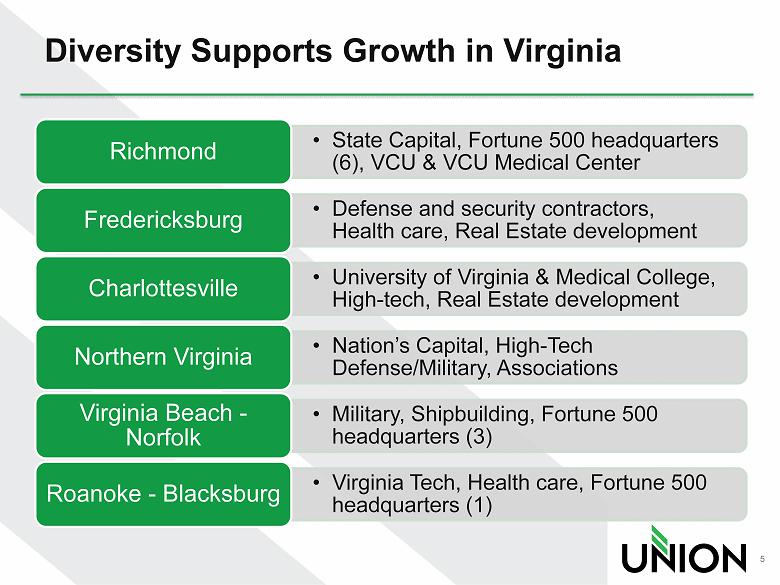

Diversity Supports Growth in Virginia 5 • State Capital, Fortune 500 headquarters (6), VCU & VCU Medical Center Richmond • Defense and security contractors, Health care, Real Estate development Fredericksburg • University of Virginia & Medical College, High - tech, Real Estate development Charlottesville • Nation’s Capital, High - Tech Defense/Military, Associations Northern Virginia • Military, Shipbuilding, Fortune 500 headquarters (3) Virginia Beach - Norfolk • Virginia Tech, Health care, Fortune 500 headquarters (1) Roanoke - Blacksburg

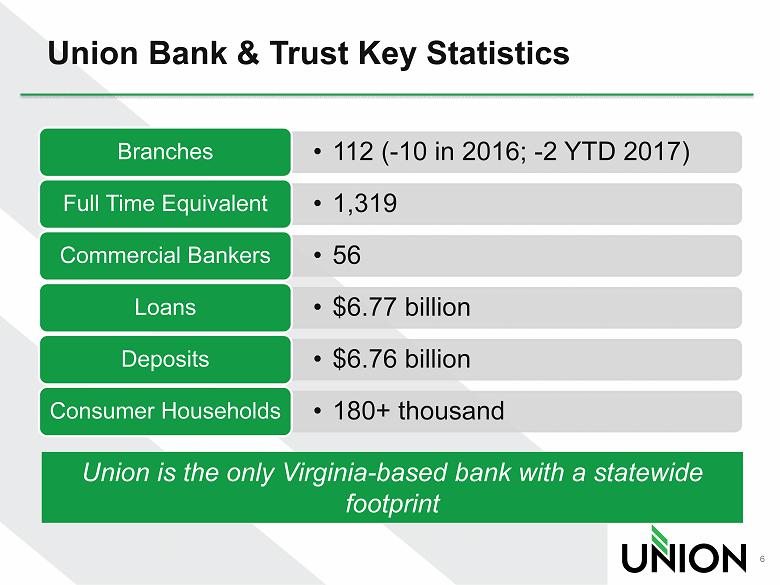

Union Bank & Trust Key Statistics • 112 ( - 10 in 2016; - 2 YTD 2017) Branches • 1,319 Full Time Equivalent • 56 Commercial Bankers • $6.77 billion Loans • $6.76 billion Deposits • 180+ thousand Consumer Households 6 Union is the only Virginia - based bank with a statewide footprint

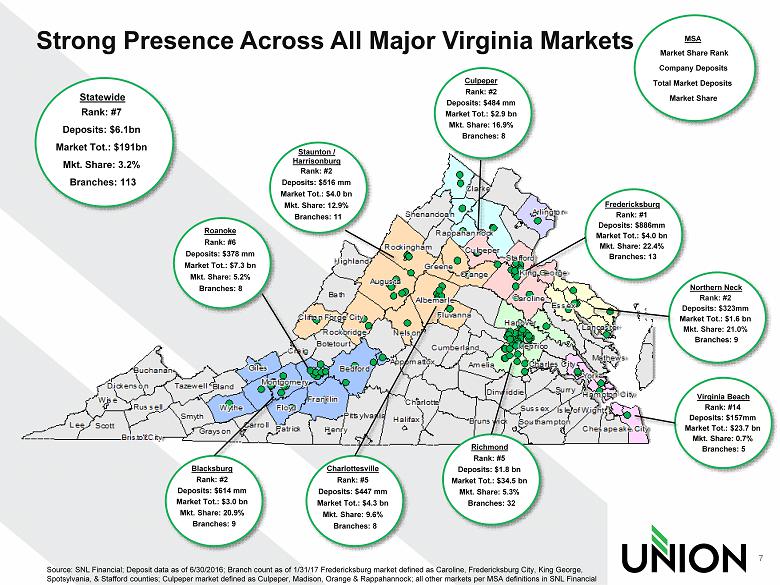

MSA Market Share Rank Company Deposits Total Market Deposits Market Share Roanoke Deposits: $378 mm Market Tot.: $7.3 bn Mkt. Share: 5.2% Rank: #6 Branches: 8 Staunton / Harrisonburg Rank: #2 Deposits: $516 mm Market Tot.: $ 4 .0 bn Mkt. Share: 12.9% Branches: 11 Blacksburg Rank: #2 Deposits: $614 mm Market Tot.: $3.0 bn Mkt. Share: 20.9% Branches: 9 Charlottesville Rank: #5 Deposits: $447 mm Market Tot.: $4.3 bn Mkt. Share: 9.6% Branches: 8 Richmond Rank: #5 Deposits: $1.8 bn Market Tot.: $34.5 bn Mkt. Share: 5.3% Branches: 32 Culpeper Rank: #2 Deposits: $484 mm Market Tot.: $2.9 bn Mkt. Share: 16.9% Branches: 8 Fredericksburg Rank: #1 Deposits: $886mm Market Tot.: $4.0 bn Mkt. Share: 22.4% Branches: 13 Statewide Rank: #7 Deposits: $6.1bn Market Tot.: $191bn Mkt. Share: 3.2% Branches: 113 Strong Presence Across All Major Virginia Markets Northern Neck Rank: #2 Deposits: $323mm Market Tot.: $1.6 bn Mkt. Share: 21.0% Branches: 9 Virginia Beach Rank: #14 Deposits: $157mm Market Tot.: $23.7 bn Mkt. Share: 0.7% Branches: 5 Source: SNL Financial; Deposit data as of 6/30/2016; Branch count as of 1/31/17 Fredericksburg market defined as Caroline, Fredericksburg City, King George, Spotsylvania, & Stafford counties; Culpeper market defined as Culpeper, Madison, Orange & Rappahannock; all other markets per MS A definitions in SNL Financial 7

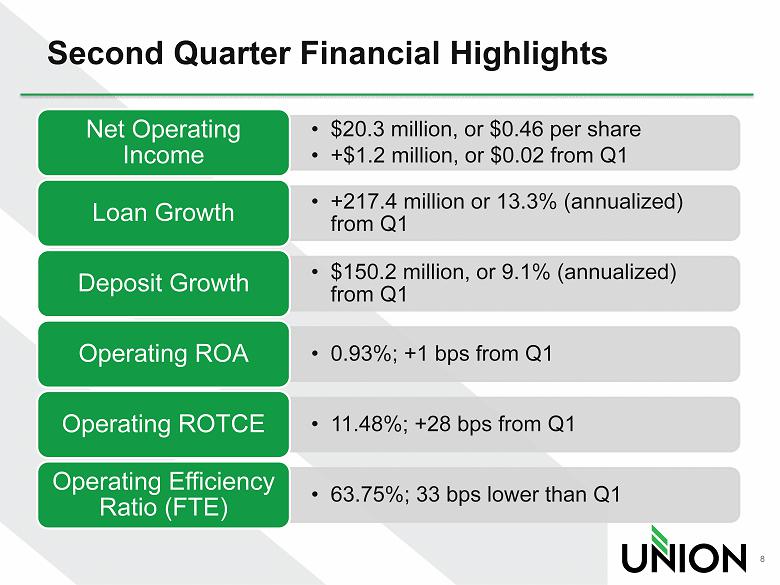

Second Quarter Financial Highlights • $20.3 million, or $0.46 per share • +$1.2 million, or $0.02 from Q1 Net Operating Income • +217.4 million or 13.3% (annualized) from Q1 Loan Growth • $150.2 million, or 9.1% (annualized) from Q1 Deposit Growth • 0.93%; +1 bps from Q1 Operating ROA • 11.48%; +28 bps from Q1 Operating ROTCE • 63.75%; 33 bps lower than Q1 Operating Efficiency Ratio (FTE) 8

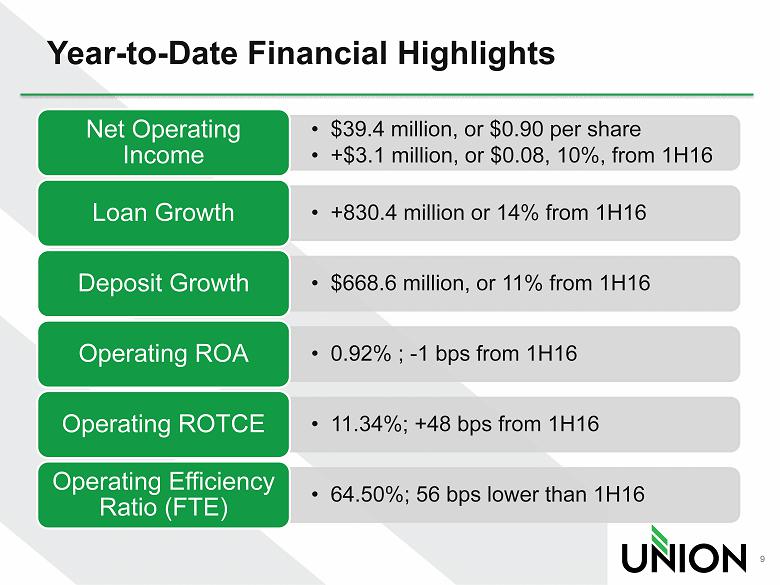

Year - to - Date Financial Highlights • $39.4 million, or $0.90 per share • +$3.1 million, or $0.08, 10%, from 1H16 Net Operating Income • +830.4 million or 14% from 1H16 Loan Growth • $668.6 million, or 11% from 1H16 Deposit Growth • 0.92% ; - 1 bps from 1H16 Operating ROA • 11.34%; +48 bps from 1H16 Operating ROTCE • 64.50%; 56 bps lower than 1H16 Operating Efficiency Ratio (FTE) 9

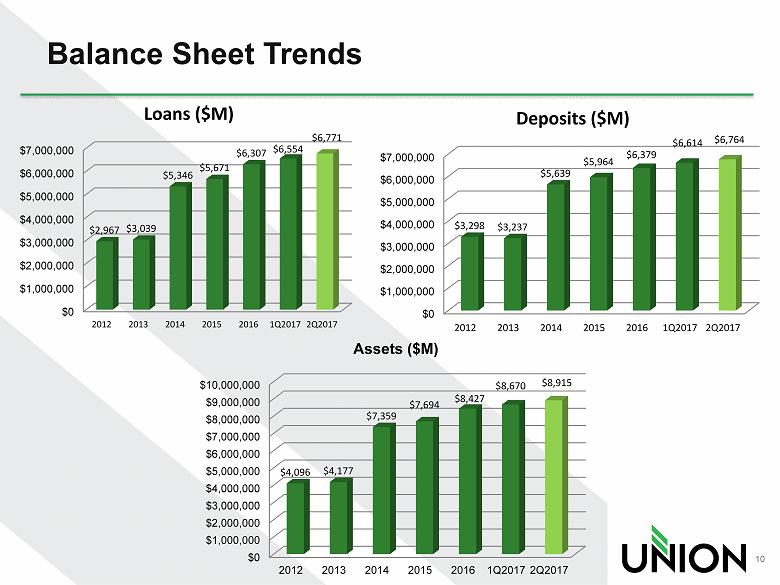

Balance Sheet Trends 10 $0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000 2012 2013 2014 2015 2016 1Q2017 2Q2017 $2,967 $3,039 $5,346 $5,671 $6,307 $6,554 $6,771 Loans ($M) $0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000 2012 2013 2014 2015 2016 1Q2017 2Q2017 $3,298 $3,237 $5,639 $5,964 $6,379 $6,614 $6,764 Deposits ($M) $0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000 $8,000,000 $9,000,000 $10,000,000 2012 2013 2014 2015 2016 1Q2017 2Q2017 $4,096 $4,177 $7,359 $7,694 $8,427 $8,670 $8,915 Assets ($M)

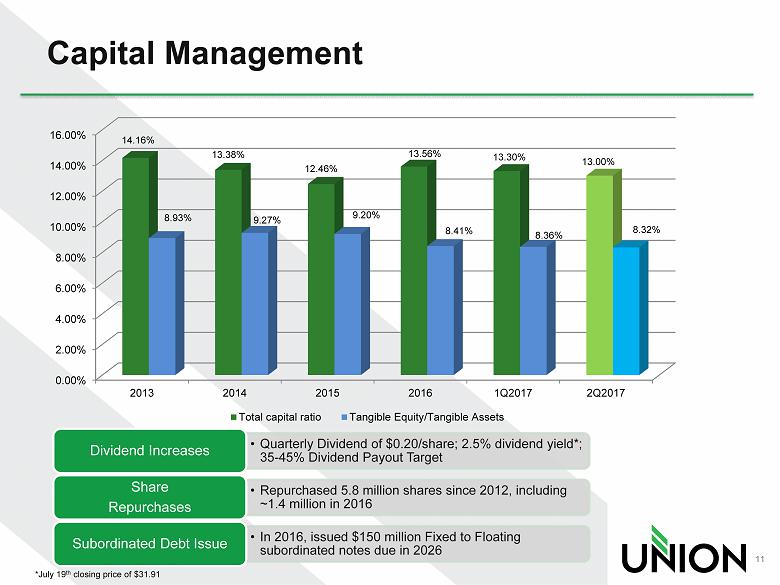

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 2013 2014 2015 2016 1Q2017 2Q2017 14.16% 13.38% 12.46% 13.56% 13.30% 13.00% 8.93% 9.27% 9.20% 8.41% 8.36% 8.32% Total capital ratio Tangible Equity/Tangible Assets Capital Management 11 • Quarterly Dividend of $0.20/share; 2.5% dividend yield*; 35 - 45% Dividend Payout Target Dividend Increases • Repurchased 5.8 million shares since 2012, including ~1.4 million in 2016 Share Repurchases • In 2016, issued $150 million Fixed to Floating subordinated notes due in 2026 Subordinated Debt Issue *July 19 th closing price of $ 31.91

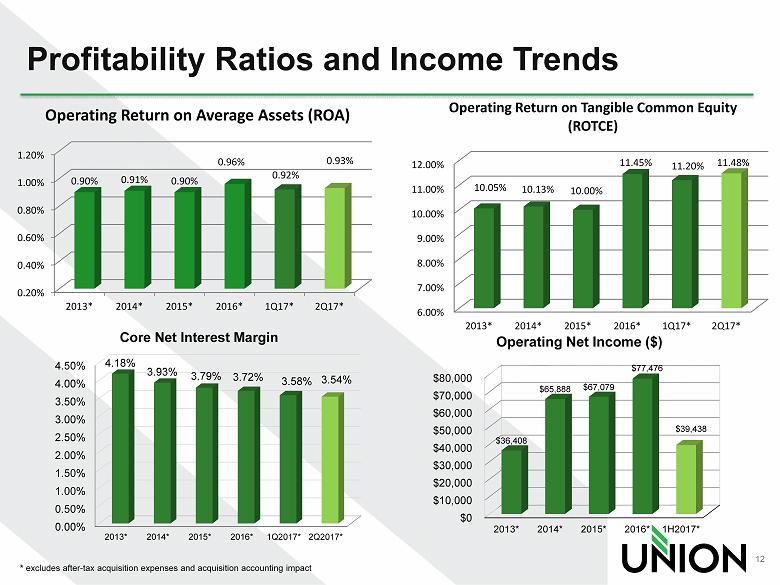

Profitability Ratios and Income Trends * excludes after - tax acquisition expenses and acquisition accounting impact 12 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 2013* 2014* 2015* 2016* 1Q17* 2Q17* 0.90% 0.91% 0.90% 0.96% 0.92% 0.93% Operating Return on Average Assets (ROA) 6.00% 7.00% 8.00% 9.00% 10.00% 11.00% 12.00% 2013* 2014* 2015* 2016* 1Q17* 2Q17* 10.05% 10.13% 10.00% 11.45% 11.20% 11.48% Operating Return on Tangible Common Equity (ROTCE) $0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 $80,000 2013* 2014* 2015* 2016* 1H2017* $36,408 $65,888 $67,079 $77,476 $39,438 Operating Net Income ($) 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50% 2013* 2014* 2015* 2016* 1Q2017* 2Q2017* 4.18% 3.93% 3.79% 3.72% 3.58% 3.54% Core Net Interest Margin

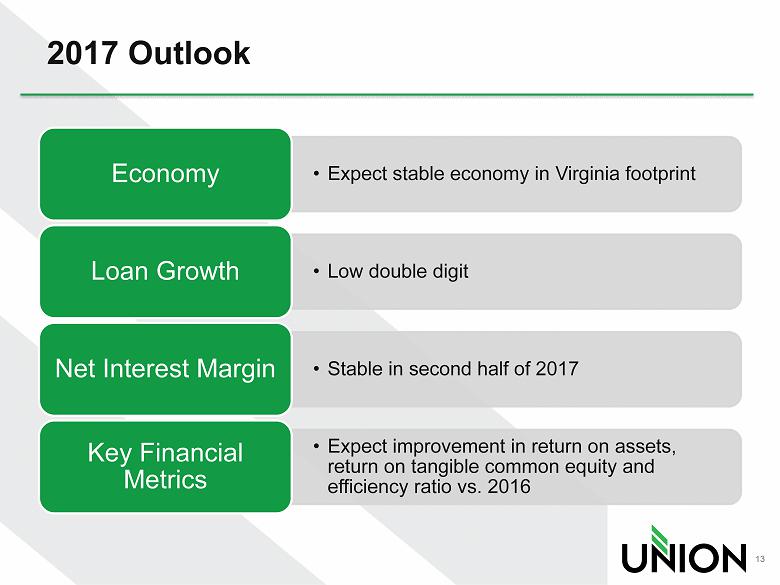

2017 Outlook • Expect stable economy in Virginia footprint Economy • Low double digit Loan Growth • Stable in second half of 2017 Net Interest Margin • Expect improvement in return on assets, return on tangible common equity and efficiency ratio vs. 2016 Key Financial Metrics 13

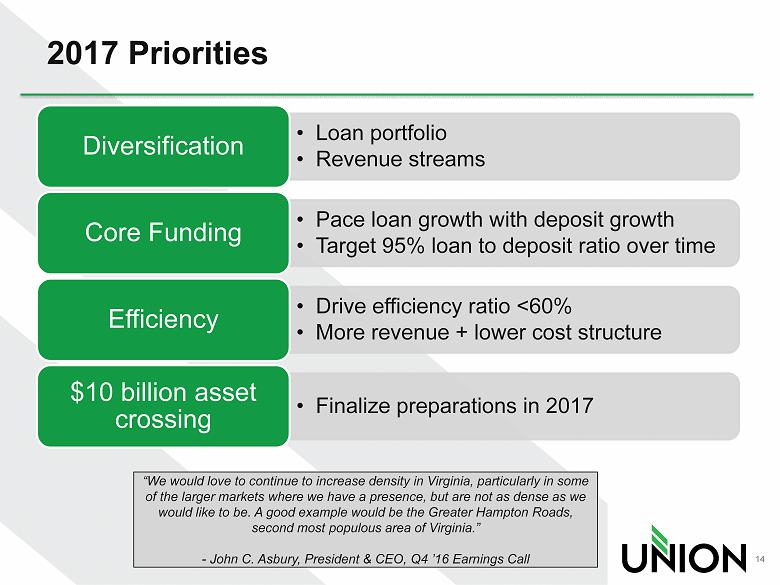

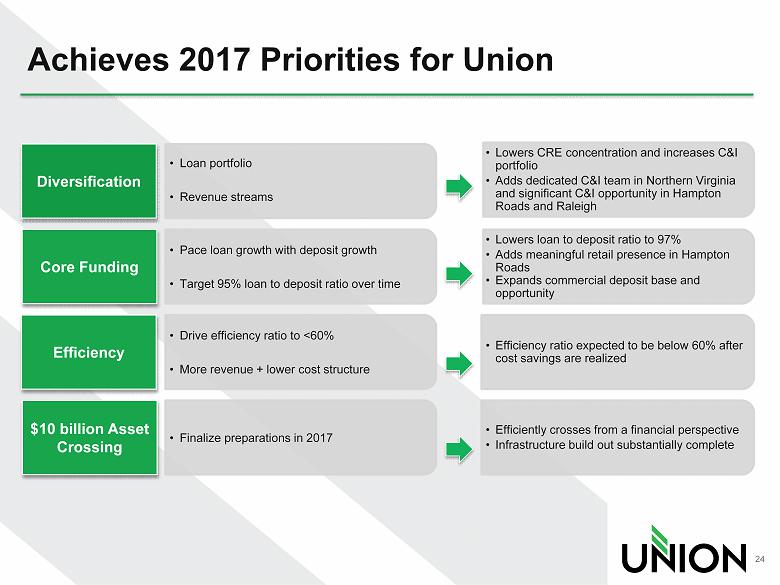

2017 Priorities 14 • Loan portfolio • Revenue streams Diversification • Pace loan growth with deposit growth • Target 95% loan to deposit ratio over time Core Funding • Drive efficiency ratio <60% • More revenue + lower cost structure Efficiency • Finalize preparations in 2017 $10 billion asset crossing “We would love to continue to increase density in Virginia, particularly in some of the larger markets where we have a presence, but are not as dense as we would like to be. A good example would be the Greater Hampton Roads, second most populous area of Virginia .” - John C. Asbury, President & CEO, Q4 ’16 Earnings Call

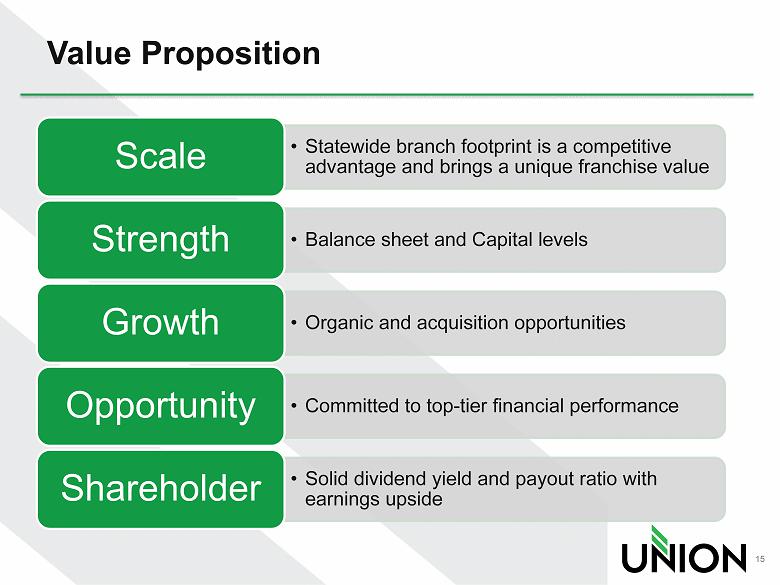

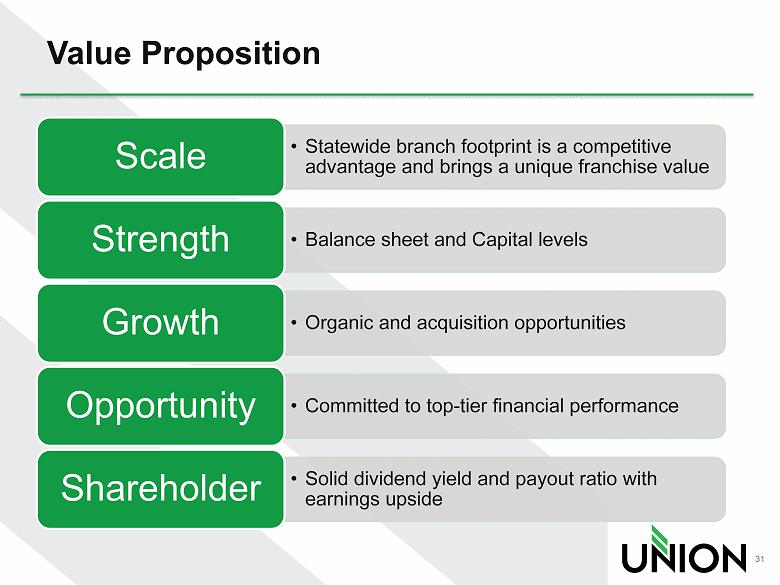

Value Proposition • Statewide branch footprint is a competitive advantage and brings a unique franchise value Scale • Balance sheet and Capital levels Strength • Organic and acquisition opportunities Growth • Committed to top - tier financial performance Opportunity • Solid dividend yield and payout ratio with earnings upside Shareholder 15

Merger Details

17 Additional Merger Information Additional Information and Where to Find It In connection with the proposed merger, Union will file with the SEC a registration statement on Form S - 4 to register the shares of Union common stock to be issued to the shareholders of Xenith. The registration statement will include a joint proxy statement of Union an d X enith and a prospectus of Union. A definitive joint proxy statement/prospectus will be sent to the shareholders of Union and Xenith seeking their a ppr oval of the merger and related matters. This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. Before making any voting or investment decision, investors and shareholders of Union and Xenith are urged to read carefully t he entire registration statement and joint proxy statement/prospectus when they become available, including any amendments there to, because they will contain important information about the proposed transaction. Free copies of these documents may be obtained as described below. Investors and shareholders of both companies are urged to read the registration statement on Form S - 4 and the joint proxy statement/prospe ctus included within the registration statement and any other relevant documents to be filed with the SEC in connection with the p rop osed merger because they will contain important information about Union, Xenith and the proposed transaction. Investors and shareholders of both com panies are urged to review carefully and consider all public filings by Union and Xenith with the SEC, including but not limited to their Annual Rep orts on Form 10 - K, their proxy statements, their Quarterly Reports on Form 10 - Q, and their Current Reports on Form 8 - K. Investors and shareholders may ob tain free copies of these documents through the website maintained by the SEC at www.sec.gov. Free copies of the joint proxy statement/prospec tus and other documents filed with the SEC also may be obtained by directing a request by telephone or mail to Union Bankshares Corporation , 1 051 East Cary Street, Suite 1200, Richmond, Virginia 23219, Attention: Investor Relations (telephone: (804) 633 - 5031), or Xenith Bankshares, Inc. 901 E. Cary Street Richmond, Virginia, 23219, Attention: Thomas W. Osgood (telephone: (804) 433 - 2200), or by accessing Union’s website at www.banka tunion.com under “Investor Relations” or Xenith’s website at www.xenithbank.com under “Investor Relations” under “About Us.” The informa tio n on Union’s and Xenith’s websites is not, and shall not be deemed to be, a part of this presentation or incorporated into other filings either company makes with the SEC . Union and Xenith and their respective directors and executive officers may be deemed to be participants in the solicitation of prox ies from the shareholders of Union and/or Xenith in connection with the merger. Information about the directors and executive officers of Uni on is set forth in the proxy statement for Union’s 2017 annual meeting of shareholders filed with the SEC on March 21, 2017. Information about the dir ectors and executive officers of Xenith is set forth in Xenith’s Annual Report on Form 10 - K, as amended, filed with the SEC on May 1, 2017. Additiona l information regarding the interests of these participants and other persons who may be deemed participants in the merger may be obtained by reading th e joint proxy statement/prospectus regarding the merger when it becomes available. Free copies of these documents may be obtained as descri bed above.

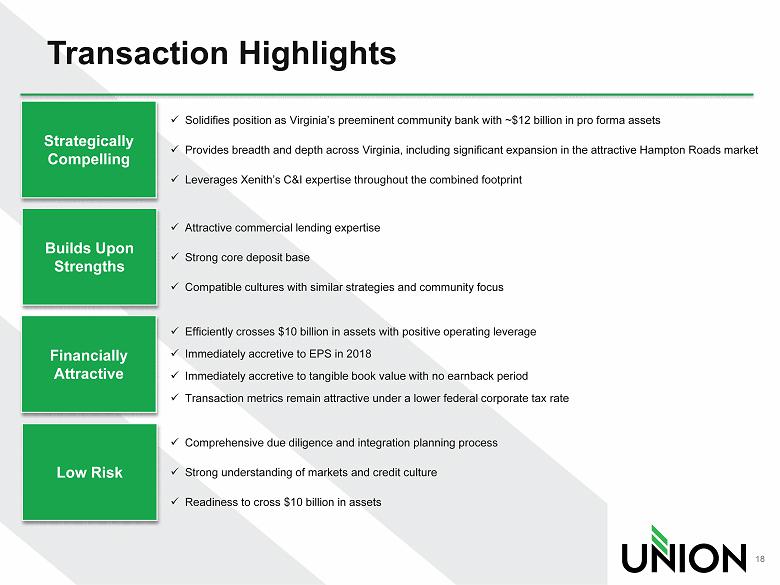

x Solidifies position as Virginia’s preeminent community bank with ~$12 billion in pro forma assets x Provides breadth and depth across Virginia, including significant expansion in the attractive Hampton Roads market x Leverages Xenith’s C&I expertise throughout the combined footprint Transaction Highlights x Attractive commercial lending expertise x Strong core deposit base x Compatible cultures with similar strategies and community focus x Efficiently crosses $10 billion in assets with positive operating leverage x Immediately accretive to EPS in 2018 x Immediately accretive to tangible book value with no earnback period x Transaction metrics remain attractive under a lower federal corporate tax rate x Comprehensive due diligence and integration planning process x Strong understanding of markets and credit culture x Readiness to cross $10 billion in assets Strategically Compelling Builds Upon Strengths Financially Attractive Low Risk 18

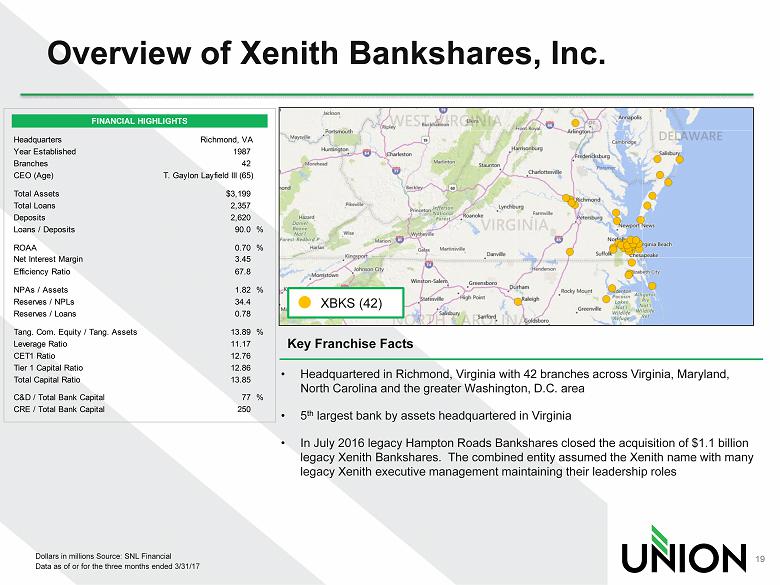

FINANCIAL HIGHLIGHTS Headquarters Richmond, VA Year Established 1987 Branches 42 CEO (Age) T. Gaylon Layfield III (65) Total Assets $3,199 Total Loans 2,357 Deposits 2,620 Loans / Deposits 90.0 % ROAA 0.70 % Net Interest Margin 3.45 Efficiency Ratio 67.8 NPAs / Assets 1.82 % Reserves / NPLs 34.4 Reserves / Loans 0.78 Tang. Com. Equity / Tang. Assets 13.89 % Leverage Ratio 11.17 CET1 Ratio 12.76 Tier 1 Capital Ratio 12.86 Total Capital Ratio 13.85 C&D / Total Bank Capital 77 % CRE / Total Bank Capital 250 Overview of Xenith Bankshares, Inc. Dollars in millions Source : SNL Financial Data as of or for the three months ended 3/31/17 • Headquartered in Richmond, Virginia with 42 branches across Virginia, Maryland, North Carolina and the greater Washington , D.C . area • 5 th largest bank by assets headquartered in Virginia • In July 2016 legacy Hampton Roads Bankshares closed the acquisition of $1.1 billion legacy Xenith Bankshares. The combined entity assumed the Xenith name with many legacy Xenith executive management maintaining their leadership roles Key Franchise Facts XBKS (42) 19

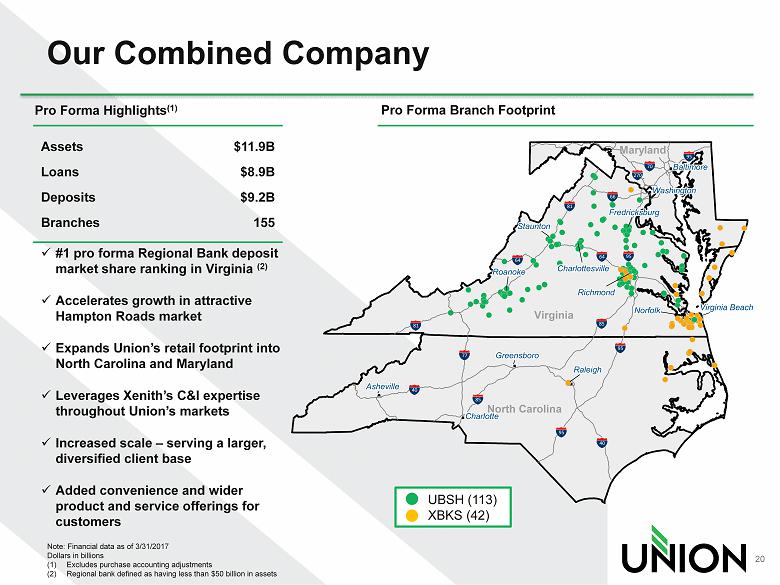

Virginia North Carolina Maryland Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Staunton Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Charlottesville Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Richmond Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Roanoke Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Fredricksburg Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Norfolk Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Raleigh Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Greensboro Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Virginia Beach Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Asheville Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Washington Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Baltimore Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte Charlotte 40 40 95 95 8 5 8 5 66 64 81 81 77 64 70 270 95 95 Our Combined Company Note: Financial data as of 3/31/2017 Dollars in billions (1) Excludes purchase accounting adjustments (2) Regional bank defined as having less than $50 billion in assets UBSH (113) XBKS (42) Pro Forma Branch Footprint Pro Forma Highlights (1) x #1 pro forma Regional Bank deposit market share ranking in Virginia (2) x Accelerates growth in attractive Hampton Roads market x Expands Union’s retail footprint into North Carolina and Maryland x Leverages Xenith’s C&I expertise throughout Union’s markets x Increased scale – serving a larger, diversified client base x Added convenience and wider product and service offerings for customers Assets $11.9B Loans $8.9B Deposits $9.2B Branches 155 20

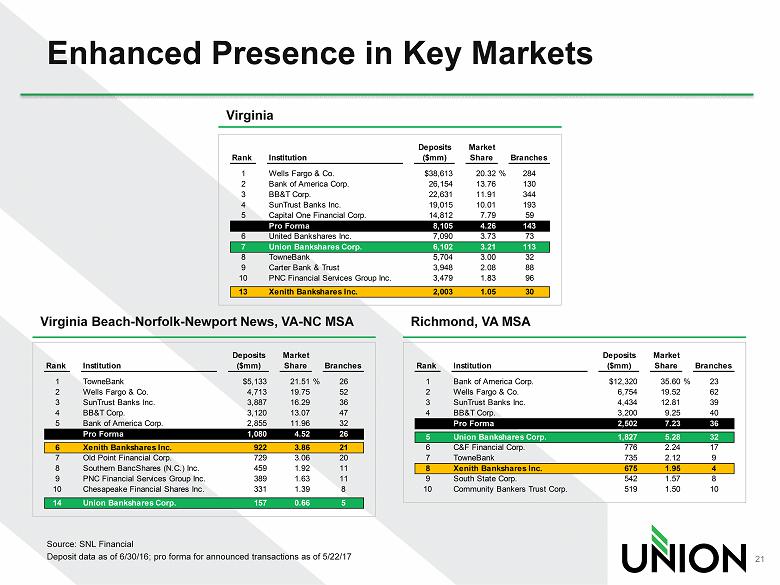

Deposits Market Rank Institution ($mm) Share Branches 1 Wells Fargo & Co. $38,613 20.32% 284 2 Bank of America Corp. 26,154 13.76 130 3 BB&T Corp. 22,631 11.91 344 4 SunTrust Banks Inc. 19,015 10.01 193 5 Capital One Financial Corp. 14,812 7.79 59 Pro Forma 8,105 4.26 143 6 United Bankshares Inc. 7,090 3.73 73 7 Union Bankshares Corp. 6,102 3.21 113 8 TowneBank 5,704 3.00 32 9 Carter Bank & Trust 3,948 2.08 88 10 PNC Financial Services Group Inc. 3,479 1.83 96 13 Xenith Bankshares Inc. 2,003 1.05 30 Enhanced Presence in Key Markets Source: SNL Financial Deposit data as of 6/30/16; pro forma for announced transactions as of 5/22/17 Virginia Beach - Norfolk - Newport News, VA - NC MSA Deposits Market Rank Institution ($mm) Share Branches 1 TowneBank $5,133 21.51% 26 2 Wells Fargo & Co. 4,713 19.75 52 3 SunTrust Banks Inc. 3,887 16.29 36 4 BB&T Corp. 3,120 13.07 47 5 Bank of America Corp. 2,855 11.96 32 Pro Forma 1,080 4.52 26 6 Xenith Bankshares Inc. 922 3.86 21 7 Old Point Financial Corp. 729 3.06 20 8 Southern BancShares (N.C.) Inc. 459 1.92 11 9 PNC Financial Services Group Inc. 389 1.63 11 10 Chesapeake Financial Shares Inc. 331 1.39 8 14 Union Bankshares Corp. 157 0.66 5 Deposits Market Rank Institution ($mm) Share Branches 1 Bank of America Corp. $12,320 35.60% 23 2 Wells Fargo & Co. 6,754 19.52 62 3 SunTrust Banks Inc. 4,434 12.81 39 4 BB&T Corp. 3,200 9.25 40 Pro Forma 2,502 7.23 36 5 Union Bankshares Corp. 1,827 5.28 32 6 C&F Financial Corp. 776 2.24 17 7 TowneBank 735 2.12 9 8 Xenith Bankshares Inc. 675 1.95 4 9 South State Corp. 542 1.57 8 10 Community Bankers Trust Corp. 519 1.50 10 Richmond, VA MSA Virginia 21

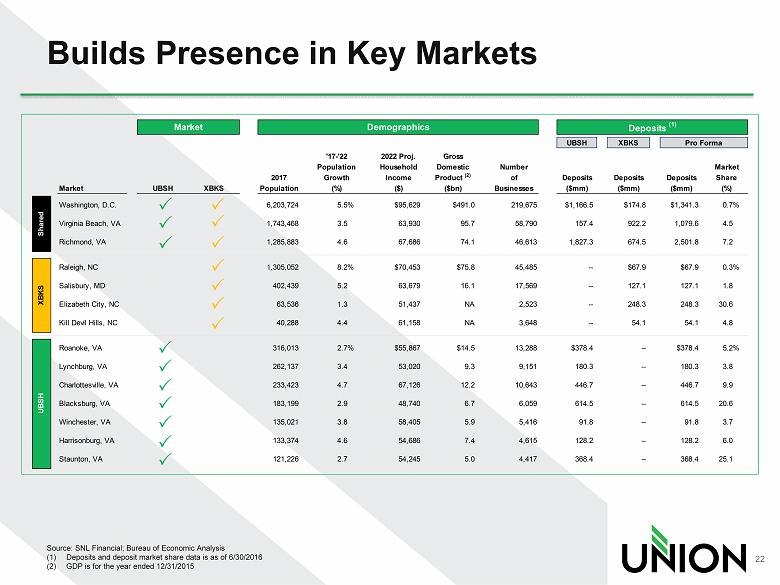

Market Demographics Deposits (1) UBSH XBKS Pro Forma '17-'22 2022 Proj. Gross Population Household Domestic Number Market 2017 Growth Income Product (2) of Deposits Deposits Deposits Share Market UBSH XBKS Population (%) ($) ($bn) Businesses ($mm) ($mm) ($mm) (%) Washington, D.C. 6,203,724 5.5% $95,629 $491.0 219,675 $1,166.5 $174.8 $1,341.3 0.7% Virginia Beach, VA 1,743,468 3.5 63,930 95.7 58,790 157.4 922.2 1,079.6 4.5 Richmond, VA 1,285,883 4.6 67,686 74.1 46,613 1,827.3 674.5 2,501.8 7.2 Raleigh, NC 1,305,052 8.2% $70,453 $75.8 45,485 -- $67.9 $67.9 0.3% Salisbury, MD 402,439 5.2 63,679 16.1 17,569 -- 127.1 127.1 1.8 Elizabeth City, NC 63,536 1.3 51,437 NA 2,523 -- 248.3 248.3 30.6 Kill Devil Hills, NC 40,288 4.4 61,158 NA 3,648 -- 54.1 54.1 4.8 Roanoke, VA 316,013 2.7% $55,867 $14.5 13,288 $378.4 -- $378.4 5.2% Lynchburg, VA 262,137 3.4 53,020 9.3 9,151 180.3 -- 180.3 3.8 Charlottesville, VA 233,423 4.7 67,126 12.2 10,643 446.7 -- 446.7 9.9 Blacksburg, VA 183,199 2.9 48,740 6.7 6,059 614.5 -- 614.5 20.6 Winchester, VA 135,021 3.8 58,405 5.9 5,416 91.8 -- 91.8 3.7 Harrisonburg, VA 133,374 4.6 54,686 7.4 4,615 128.2 -- 128.2 6.0 Staunton, VA 121,226 2.7 54,245 5.0 4,417 368.4 -- 368.4 25.1 UBSH XBKS Shared Builds Presence in Key Markets Source: SNL Financial; Bureau of Economic Analysis (1) Deposits and deposit market share data is as of 6/30/2016 (2) GDP is for the year ended 12/31/2015 22

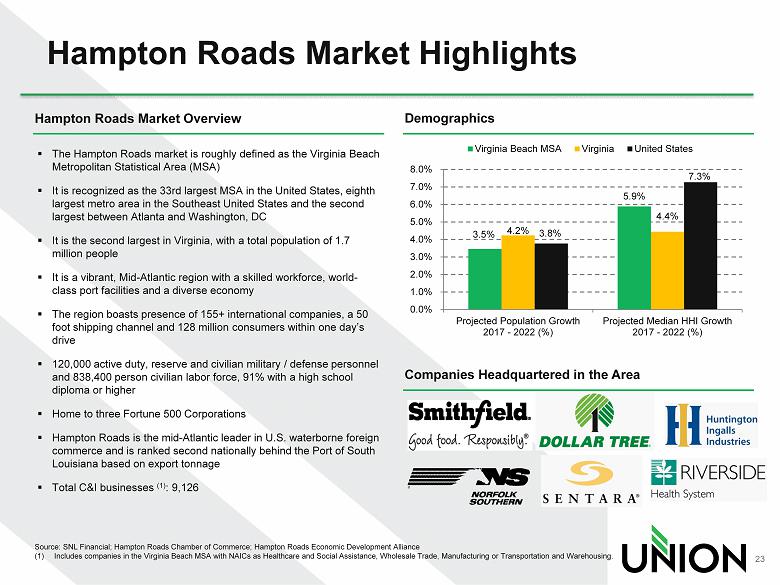

Hampton Roads Market Highlights Source: SNL Financial; Hampton Roads Chamber of Commerce; Hampton Roads Economic Development Alliance (1) Includes companies in the Virginia Beach MSA with NAICs as Healthcare and Social Assistance, Wholesale Trade, Manufacturing o r T ransportation and Warehousing. Demographics Hampton Roads Market Overview ▪ The Hampton Roads market is roughly defined as the Virginia Beach Metropolitan Statistical Area (MSA) ▪ It is recognized as the 33rd largest MSA in the United States, eighth largest metro area in the Southeast United States and the second largest between Atlanta and Washington, DC ▪ It is the second largest in Virginia, with a total population of 1.7 million people ▪ It is a vibrant, Mid - Atlantic region with a skilled workforce, world - class port facilities and a diverse economy ▪ The region boasts presence of 155+ international companies, a 50 foot shipping channel and 128 million consumers within one day’s drive ▪ 120,000 active duty, reserve and civilian military / defense personnel and 838,400 person civilian labor force, 91% with a high school diploma or higher ▪ Home to three Fortune 500 Corporations ▪ Hampton Roads is the mid - Atlantic leader in U.S. waterborne foreign commerce and is ranked second nationally behind the Port of South Louisiana based on export tonnage ▪ Total C&I businesses (1) : 9,126 3.5% 5.9% 4.2% 4.4% 3.8% 7.3% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% Projected Population Growth 2017 - 2022 (%) Projected Median HHI Growth 2017 - 2022 (%) Virginia Beach MSA Virginia United States Companies Headquartered in the Area 23

Achieves 2017 Priorities for Union • Lowers CRE concentration and increases C&I portfolio • Adds dedicated C&I team in Northern Virginia and significant C&I opportunity in Hampton Roads and Raleigh • Lowers loan to deposit ratio to 97% • Adds meaningful retail presence in Hampton Roads • Expands commercial deposit base and opportunity • Efficiency ratio expected to be below 60% after cost savings are realized • Efficiently crosses from a financial perspective • Infrastructure build out substantially complete Diversification Core Funding Efficiency $10 billion Asset Crossing • Loan portfolio • Revenue streams • Pace loan growth with deposit growth • Target 95% loan to deposit ratio over time • Drive efficiency ratio to <60 % • More revenue + lower cost structure • Finalize preparations in 2017 24

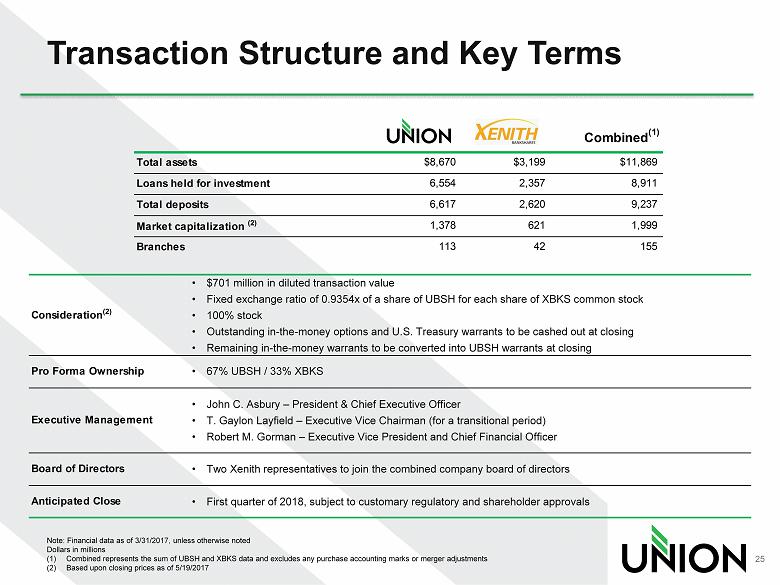

Consideration (2) Pro Forma Ownership Executive Management Board of Directors Anticipated Close Transaction Structure and Key Terms Note: Financial data as of 3/31/2017, unless otherwise noted Dollars in millions (1) Combined represents the sum of UBSH and XBKS data and excludes any purchase accounting marks or merger adjustments (2) Based upon closing prices as of 5/19/2017 Combined (1) Total assets $8,670 $3,199 $11,869 Loans held for investment 6,554 2,357 8,911 Total deposits 6,617 2,620 9,237 Market capitalization (2) 1,378 621 1,999 Branches 113 42 155 • $701 million in diluted transaction value • Fixed exchange ratio of 0.9354x of a share of UBSH for each share of XBKS common stock • 100% stock • Outstanding in - the - money options and U.S. Treasury warrants to be cashed out at closing • Remaining in - the - money warrants to be converted into UBSH warrants at closing • 67% UBSH / 33% XBKS • John C. Asbury – President & Chief Executive Officer • T. Gaylon Layfield – Executive Vice Chairman (for a transitional period) • Robert M. Gorman – Executive Vice President and Chief Financial Officer • Two Xenith representatives to join the combined company board of directors • First quarter of 2018, subject to customary regulatory and shareholder approvals 25

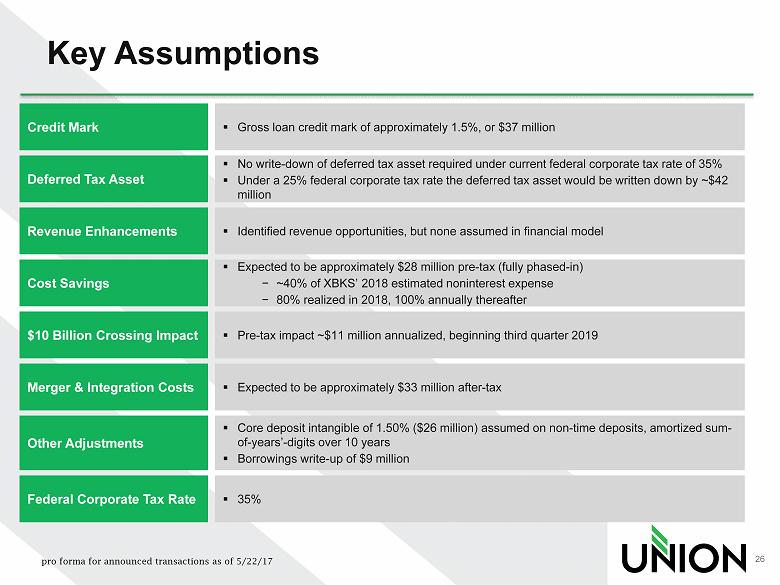

Key Assumptions Cost Savings Credit Mark ▪ Gross loan credit mark of approximately 1.5%, or $37 million ▪ Expected to be approximately $28 million pre - tax (fully phased - in) − ~40 % of XBKS ’ 2018 estimated noninterest expense − 80% realized in 2018, 100% annually thereafter Merger & Integration Costs ▪ Expected to be approximately $33 million after - tax $10 Billion Crossing Impact ▪ Pre - tax impact ~$11 million annualized, beginning third quarter 2019 Other Adjustments ▪ Core deposit intangible of 1.50% ($26 million) assumed on non - time deposits, amortized sum - of - years’ - digits over 10 years ▪ Borrowings write - up of $9 million Deferred Tax Asset ▪ No write - down of deferred tax asset required under current federal corporate tax rate of 35% ▪ Under a 25% federal corporate tax rate the deferred tax asset would be written down by ~$42 million Revenue Enhancements ▪ Identified revenue opportunities, but none assumed in financial model F ederal Corporate Tax Rate ▪ 3 5% 26 pro forma for announced transactions as of 5/22/17

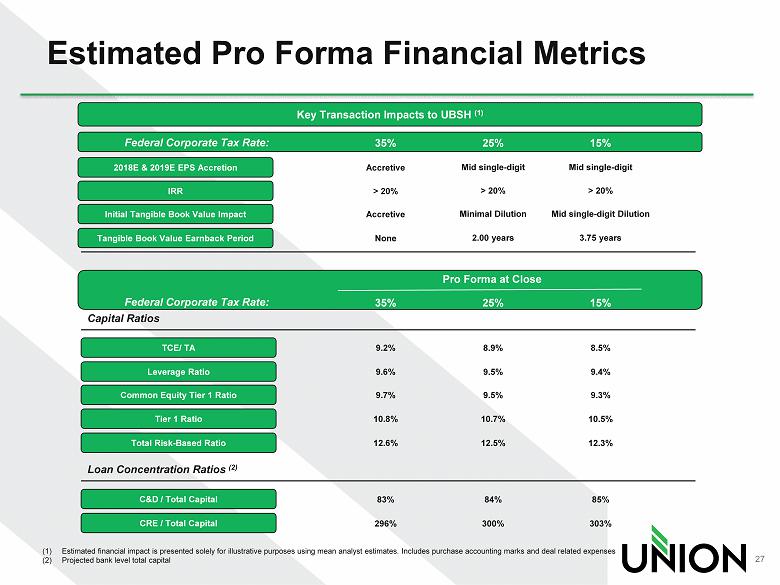

Estimated Pro Forma Financial Metrics (1) Estimated financial impact is presented solely for illustrative purposes using mean analyst estimates. Includes purchase acco unt ing marks and deal related expenses (2) Projected bank level total capital Key Transaction Impacts to UBSH (1) 2018E & 2019E EPS Accretion IRR Initial Tangible Book Value Impact Tangible Book Value Earnback Period Capital Ratios TCE/ TA Leverage Ratio Common Equity Tier 1 Ratio Tier 1 Ratio Total Risk - Based Ratio Loan Concentration Ratios (2) C&D / Total Capital CRE / Total Capital Accretive > 20% Accretive None 9.2% 9.6% 9.7% 10.8% 12.6% 8 .9% 9.5% 9.5% 10.7% 12.5% 8.5% 9.4% 9.3% 10.5% 12.3% 83% 296% 84% 300% 85% 303% Pro Forma at Close 35% Federal Corporate Tax Rate: 25% 1 5% Mid single - digit > 20% Minimal Dilution 2.00 years Mid single - digit > 20% Mid single - digit Dilution 3.75 years 35% Federal Corporate Tax Rate: 25% 1 5% 27

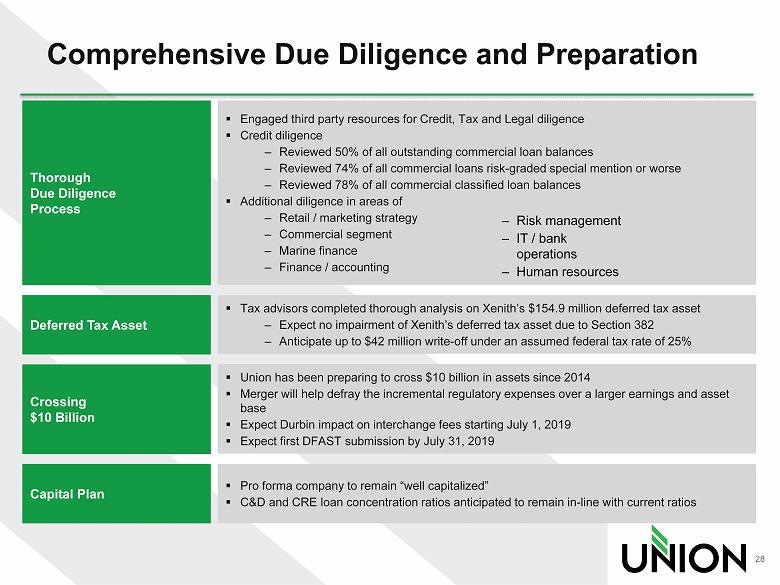

Comprehensive Due Diligence and Preparation Deferred Tax Asset ▪ Tax advisors completed thorough analysis on Xenith’s $154.9 million deferred tax asset ‒ Expect no impairment of Xenith’s deferred tax asset due to Section 382 ‒ Anticipate up to $42 million write - off under an assumed federal tax rate of 25% Thorough Due Diligence Process ▪ Engaged third party resources for Credit, Tax and Legal diligence ▪ Credit diligence ‒ Reviewed 50% of all outstanding commercial loan balances ‒ Reviewed 74% of all commercial loans risk - graded special mention or worse ‒ Reviewed 78% of all commercial classified loan balances ▪ Additional diligence in areas of ‒ Retail / marketing strategy ‒ Commercial segment ‒ Marine finance ‒ Finance / accounting Crossing $10 Billion ▪ Union has been preparing to cross $10 billion in assets since 2014 ▪ Merger will help defray the incremental regulatory expenses over a larger earnings and asset base ▪ Expect Durbin impact on interchange fees starting July 1, 2019 ▪ Expect first DFAST submission by July 31, 2019 ‒ Risk management ‒ IT / bank operations ‒ Human resources Capital Plan ▪ Pro forma company to remain “well capitalized” ▪ C&D and CRE loan concentration ratios anticipated to remain in - line with current ratios 28

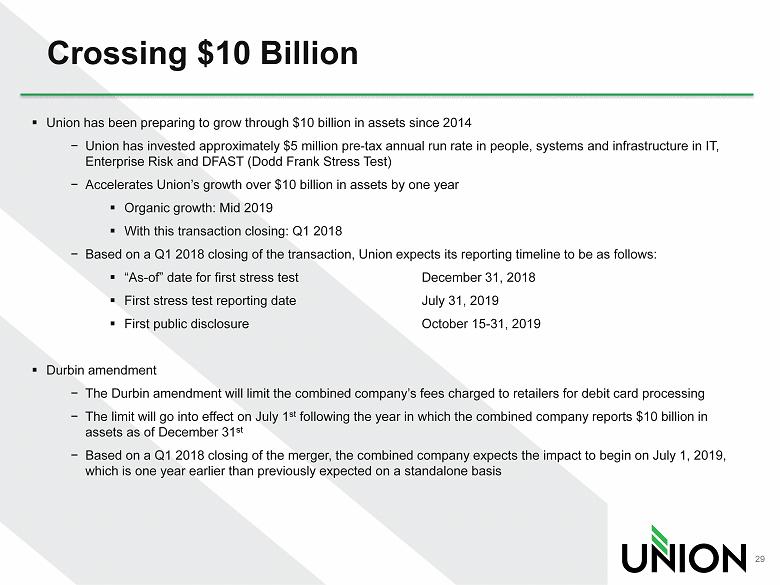

▪ Union has been preparing to grow through $10 billion in assets since 2014 − Union has invested approximately $5 million pre - tax annual run rate in people, systems and infrastructure in IT, Enterprise Risk and DFAST (Dodd Frank Stress Test) − Accelerates Union’s growth over $10 billion in assets by one year ▪ Organic growth: Mid 2019 ▪ With this transaction closing: Q1 2018 − Based on a Q1 2018 closing of the transaction, Union expects its reporting timeline to be as follows: ▪ “As - of” date for first stress test December 31, 2018 ▪ First stress test reporting date July 31, 2019 ▪ First public disclosure October 15 - 31, 2019 ▪ Durbin amendment − The Durbin amendment will limit the combined company’s fees charged to retailers for debit card processing − The limit will go into effect on July 1 st following the year in which the combined company reports $10 billion in assets as of December 31 st − Based on a Q1 2018 closing of the merger, the combined company expects the impact to begin on July 1, 2019, which is one year earlier than previously expected on a standalone basis Crossing $10 Billion 29

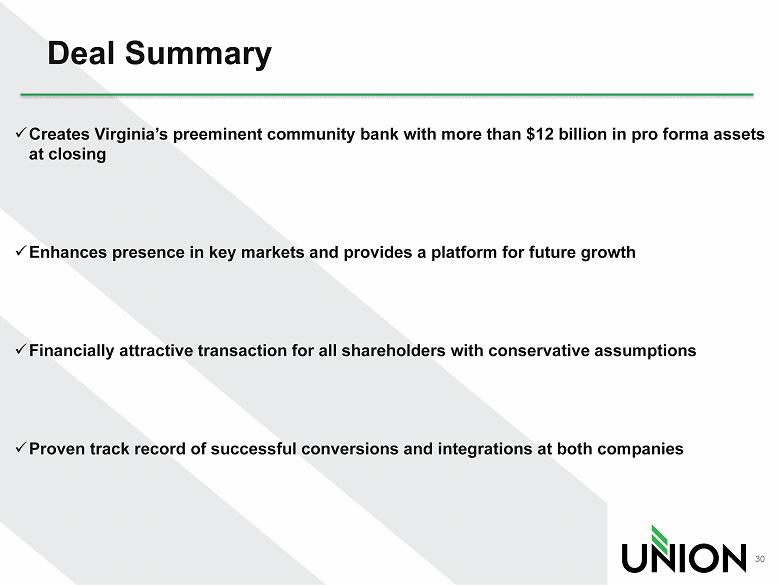

x Creates Virginia’s preeminent community bank with more than $12 billion in pro forma assets at closing x Enhances presence in key markets and provides a platform for future growth x Financially attractive transaction for all shareholders with conservative assumptions x Proven track record of successful conversions and integrations at both companies Deal Summary 30

Value Proposition • Statewide branch footprint is a competitive advantage and brings a unique franchise value Scale • Balance sheet and Capital levels Strength • Organic and acquisition opportunities Growth • Committed to top - tier financial performance Opportunity • Solid dividend yield and payout ratio with earnings upside Shareholder 31

APPENDIX 32

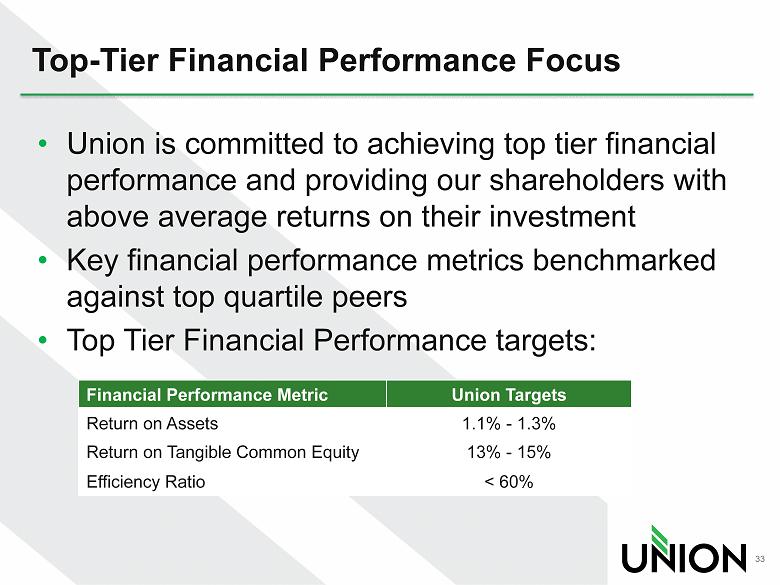

Top - Tier Financial Performance Focus • Union is committed to achieving top tier financial performance and providing our shareholders with above average returns on their investment • Key financial performance metrics benchmarked against top quartile peers • Top Tier Financial Performance targets: 33 Financial Performance Metric Union Targets Return on Assets 1.1% - 1.3% Return on Tangible Common Equity 13% - 15% Efficiency Ratio < 60%

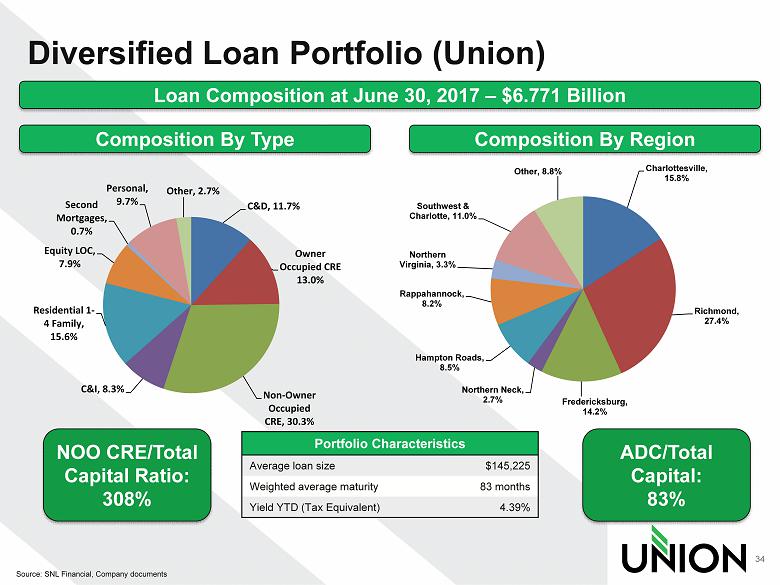

Diversified Loan Portfolio (Union) 34 Source: SNL Financial, Company documents Loan Composition at June 30, 2017 – $6.771 Billion Portfolio Characteristics Average loan size $145,225 Weighted average maturity 83 months Yield YTD (Tax Equivalent) 4.39% Composition By Type Composition By Region NOO CRE/Total Capital Ratio: 308% ADC/Total Capital: 83% C&D, 11.7% Owner Occupied CRE 13.0% Non - Owner Occupied CRE, 30.3% C&I, 8.3% Residential 1 - 4 Family , 15.6% Equity LOC, 7.9% Second Mortgages , 0.7% Personal , 9.7% Other, 2.7% Charlottesville , 15.8% Richmond , 27.4% Fredericksburg , 14.2% Northern Neck , 2.7% Hampton Roads , 8.5% Rappahannock , 8.2% Northern Virginia , 3.3% Southwest & Charlotte , 11.0% Other, 8.8%

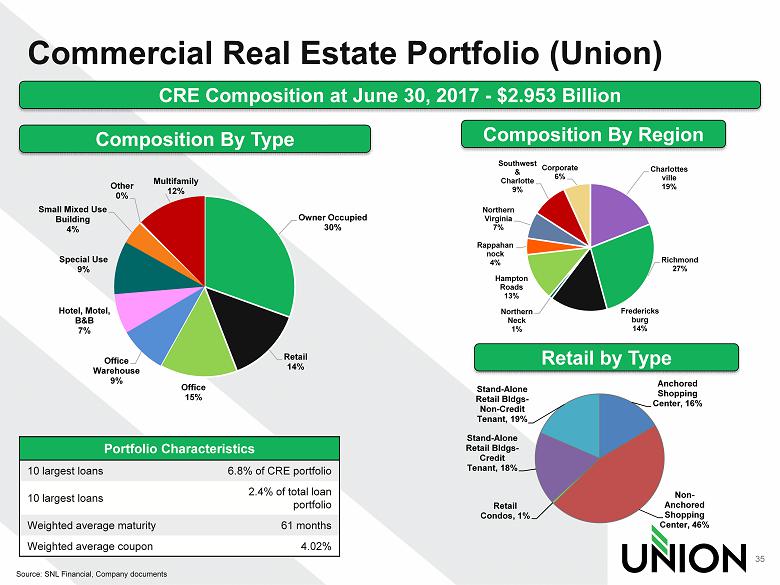

Commercial Real Estate Portfolio (Union) 35 Source: SNL Financial, Company documents CRE Composition at June 30, 2017 - $2.953 Billion Portfolio Characteristics 10 largest loans 6.8% of CRE portfolio 10 largest loans 2.4% of total loan portfolio Weighted average maturity 61 months Weighted average coupon 4.02% Composition By Type Composition By Region Owner Occupied 30% Retail 14% Office 15% Office Warehouse 9% Hotel, Motel, B&B 7% Special Use 9% Small Mixed Use Building 4% Other 0% Multifamily 12% Charlottes ville 19% Richmond 27% Fredericks burg 14% Northern Neck 1% Hampton Roads 13% Rappahan nock 4% Northern Virginia 7% Southwest & Charlotte 9% Corporate 6% Anchored Shopping Center, 16% Non - Anchored Shopping Center, 46% Retail Condos, 1% Stand - Alone Retail Bldgs - Credit Tenant, 18% Stand - Alone Retail Bldgs - Non - Credit Tenant, 19% Retail by Type

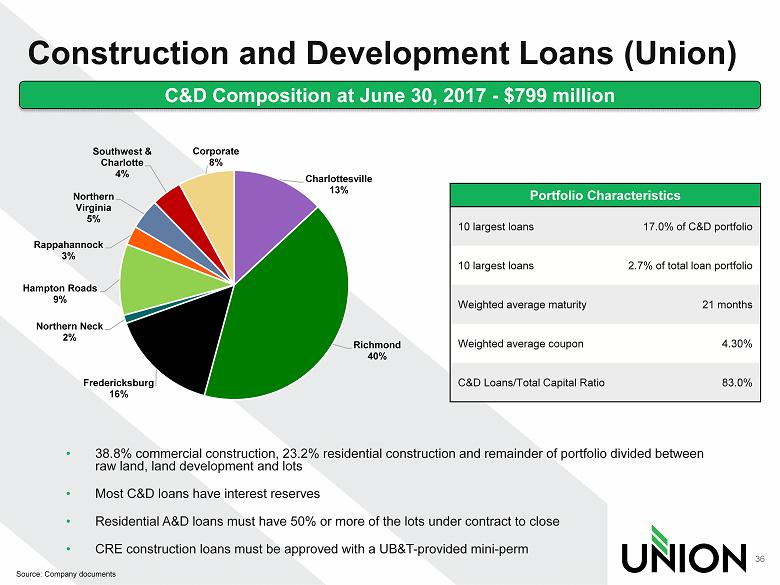

Construction and Development Loans (Union) 36 Source: Company documents C&D Composition at June 30, 2017 - $799 million Portfolio Characteristics 10 largest loans 17.0% of C&D portfolio 10 largest loans 2.7% of total loan portfolio Weighted average maturity 21 months Weighted average coupon 4.30% C&D Loans/Total Capital Ratio 83.0 % • 38.8% commercial construction, 23.2% residential construction and remainder of portfolio divided between raw land, land development and lots • Most C&D loans have interest reserves • Residential A&D loans must have 50 % or more of the lots under contract to close • CRE construction loans must be approved with a UB&T - provided mini - perm Charlottesville 13% Richmond 40% Fredericksburg 16% Northern Neck 2% Hampton Roads 9% Rappahannock 3% Northern Virginia 5% Southwest & Charlotte 4% Corporate 8%

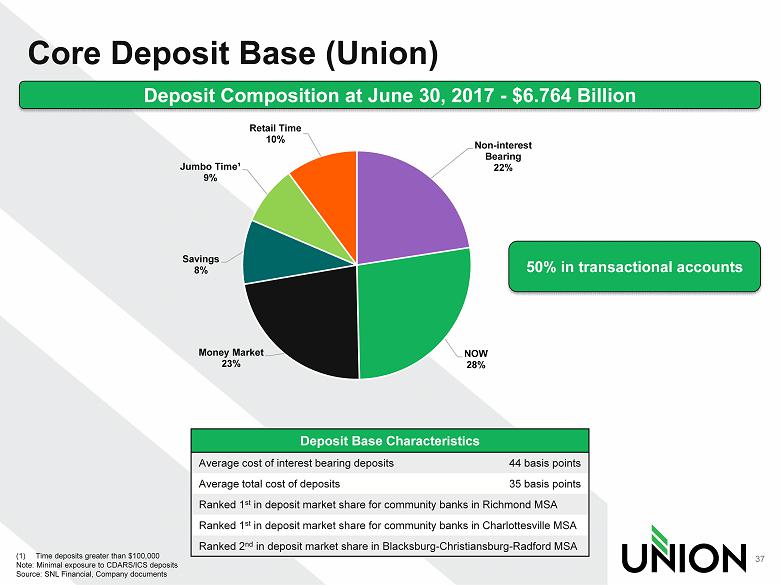

Core Deposit Base (Union) 37 (1) Time deposits greater than $100,000 Note: Minimal exposure to CDARS/ICS deposits Source: SNL Financial, Company documents Deposit Composition at June 30, 2017 - $6.764 Billion Deposit Base Characteristics Average cost of interest bearing deposits 44 basis points Average total cost of deposits 35 basis points Ranked 1 st in deposit market share for community banks in Richmond MSA Ranked 1 st in deposit market share for community banks in Charlottesville MSA Ranked 2 nd in deposit market share in Blacksburg - Christiansburg - Radford MSA 50% in transactional accounts Non - interest Bearing 22% NOW 28% Money Market 23% Savings 8% Jumbo Time¹ 9% Retail Time 10%

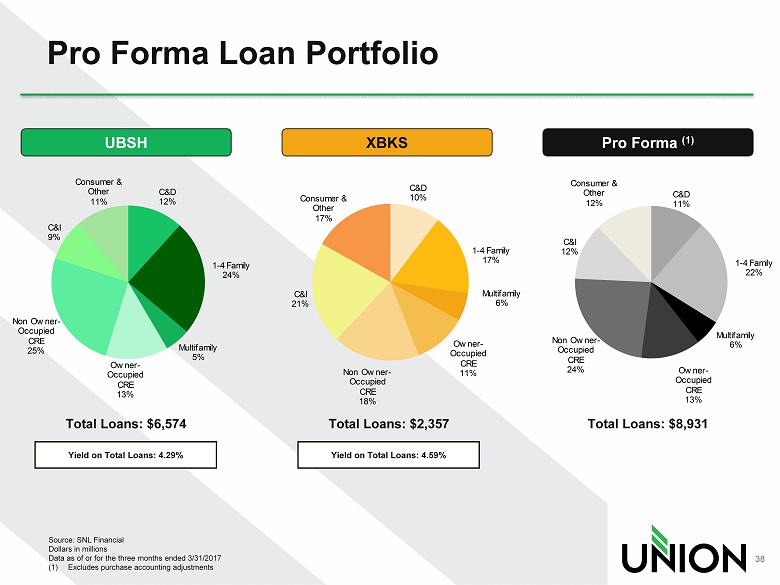

C&D 12% 1 - 4 Family 24% Multifamily 5% Owner - Occupied CRE 13% Non Owner - Occupied CRE 25% C&I 9% Consumer & Other 11% Pro Forma Loan Portfolio Source: SNL Financial Dollars in millions Data as of or for the three months ended 3/31/2017 (1) Excludes purchase accounting adjustments UBSH XBKS Pro Forma (1) C&D 10% 1 - 4 Family 17% Multifamily 6% Owner - Occupied CRE 11% Non Owner - Occupied CRE 18% C&I 21% Consumer & Other 17% C&D 11% 1 - 4 Family 22% Multifamily 6% Owner - Occupied CRE 13% Non Owner - Occupied CRE 24% C&I 12% Consumer & Other 12% Yield on Total Loans: 4.29% Yield on Total Loans : 4.59% Total Loans: $6,574 Total Loans: $2,357 Total Loans: $8,931 38

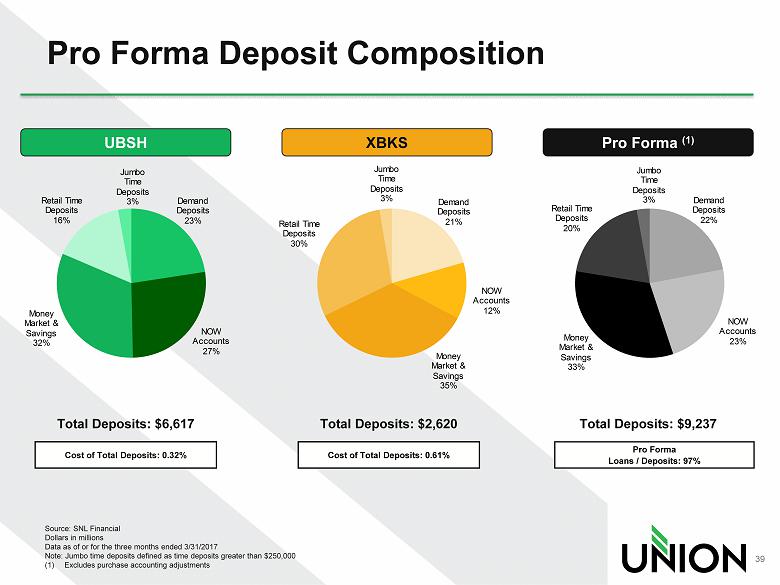

Pro Forma Deposit Composition Source: SNL Financial Dollars in millions Data as of or for the three months ended 3/31/2017 Note: Jumbo time deposits defined as time deposits greater than $250,000 (1) Excludes purchase accounting adjustments UBSH XBKS Pro Forma (1) Demand Deposits 23% NOW Accounts 27% Money Market & Savings 32% Retail Time Deposits 16% Jumbo Time Deposits 3% Demand Deposits 21% NOW Accounts 12% Money Market & Savings 35% Retail Time Deposits 30% Jumbo Time Deposits 3% Cost of Total Deposits: 0.32% Cost of Total Deposits: 0.61% Demand Deposits 22% NOW Accounts 23% Money Market & Savings 33% Retail Time Deposits 20% Jumbo Time Deposits 3% Total Deposits: $6,617 Total Deposits: $2,620 Total Deposits: $9,237 Pro Forma Loans / Deposits: 97% 39

Non - GAAP Measures In reporting the results of the quarter ended June 30, 2017, and in prior periods, the Company has provided supplemental performance measures on a tax - equivalent, tangible, or operating basis. These measures are a supplement to GAAP used to prepare the Company’s financial statements and should not be considered in isolation or as a substitute for comparable measures calculated in accordance with GAAP. In addition, the Company’s non - GAAP measures may not be comparable to non - GAAP measures of other companies. Net interest income (FTE), which is used in computing net interest margin (FTE), provides valuable additional insight into the net interest margin by adjusting for differences in tax treatment of interest income sources. Core net interest income (FTE), which is used in computing core net interest margin (FTE), provides valuable additional insight into the net interest margin by adjusting for differences in tax treatment of interest income sources as well as the net accretion of acquisition - related fair value marks. The Company believes tangible common equity is an important indication of its ability to grow organically and through business combinations as well as its ability to pay dividends and to engage in various capital management strategies. Tangible common equity is used in the calculation of certain profitability, capital, and per share ratios. These ratios are meaningful measures of capital adequacy because they provide a meaningful base for period - to - period and company - to - company comparisons, which the Company believes will assist investors in assessing the capital of the Company and its ability to absorb potential losses . 40

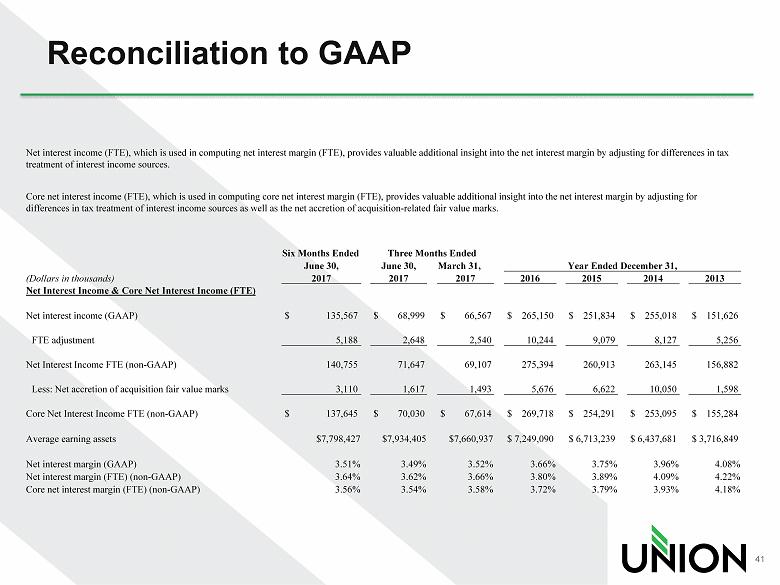

Reconciliation to GAAP Net interest income (FTE), which is used in computing net interest margin (FTE), provides valuable additional insight into th e n et interest margin by adjusting for differences in tax treatment of interest income sources. Core net interest income (FTE), which is used in computing core net interest margin (FTE), provides valuable additional insig ht into the net interest margin by adjusting for differences in tax treatment of interest income sources as well as the net accretion of acquisition - related fair value marks. Six Months Ended Three Months Ended June 30, June 30, March 31, Year Ended December 31, (Dollars in thousands) 2017 2017 2017 2016 2015 2014 2013 Net Interest Income & Core Net Interest Income (FTE) Net interest income (GAAP) $ 135,567 $ 68,999 $ 66,567 $ 265,150 $ 251,834 $ 255,018 $ 151,626 FTE adjustment 5,188 2,648 2,540 10,244 9,079 8,127 5,256 Net Interest Income FTE (non - GAAP) 140,755 71,647 69,107 275,394 260,913 263,145 156,882 Less: Net accretion of acquisition fair value marks 3,110 1,617 1,493 5,676 6,622 10,050 1,598 Core Net Interest Income FTE (non - GAAP) $ 137,645 $ 70,030 $ 67,614 $ 269,718 $ 254,291 $ 253,095 $ 155,284 Average earning assets $7,798,427 $7,934,405 $7,660,937 $ 7,249,090 $ 6,713,239 $ 6,437,681 $ 3,716,849 Net interest margin (GAAP) 3.51% 3.49% 3.52% 3.66% 3.75% 3.96% 4.08% Net interest margin (FTE) (non - GAAP) 3.64% 3.62% 3.66% 3.80% 3.89% 4.09% 4.22% Core net interest margin (FTE) (non - GAAP) 3.56% 3.54% 3.58% 3.72% 3.79% 3.93% 4.18% 41

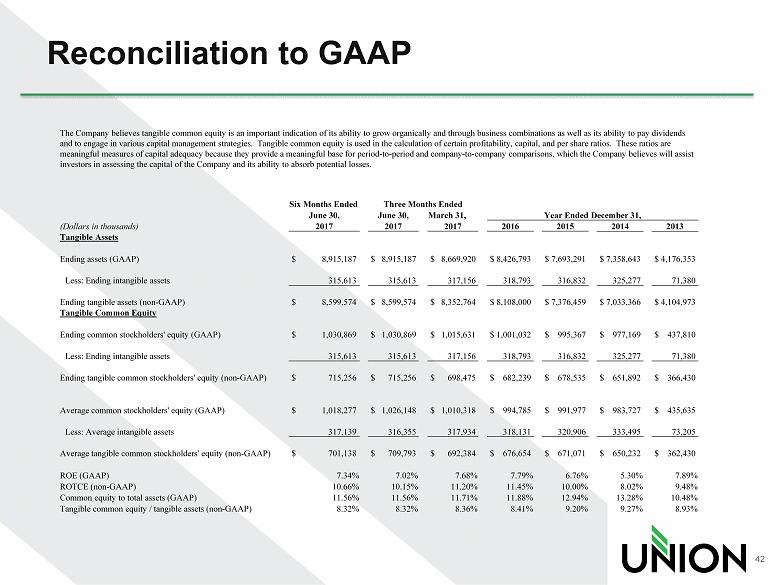

Reconciliation to GAAP The Company believes tangible common equity is an important indication of its ability to grow organically and through busines s c ombinations as well as its ability to pay dividends and to engage in various capital management strategies. Tangible common equity is used in the calculation of certain profita bil ity, capital, and per share ratios. These ratios are meaningful measures of capital adequacy because they provide a meaningful base for period - to - period and company - to - company compa risons, which the Company believes will assist investors in assessing the capital of the Company and its ability to absorb potential losses. Six Months Ended Three Months Ended June 30, June 30, March 31, Year Ended December 31, (Dollars in thousands) 2017 2017 2017 2016 2015 2014 2013 Tangible Assets Ending assets (GAAP) $ 8,915,187 $ 8,915,187 $ 8,669,920 $ 8,426,793 $ 7,693,291 $ 7,358,643 $ 4,176,353 Less: Ending intangible assets 315,613 315,613 317,156 318,793 316,832 325,277 71,380 Ending tangible assets (non - GAAP) $ 8,599,574 $ 8,599,574 $ 8,352,764 $ 8,108,000 $ 7,376,459 $ 7,033,366 $ 4,104,973 Tangible Common Equity Ending common stockholders' equity (GAAP) $ 1,030,869 $ 1,030,869 $ 1,015,631 $ 1,001,032 $ 995,367 $ 977,169 $ 437,810 Less: Ending intangible assets 315,613 315,613 317,156 318,793 316,832 325,277 71,380 Ending tangible common stockholders' equity (non - GAAP) $ 715,256 $ 715,256 $ 698,475 $ 682,239 $ 678,535 $ 651,892 $ 366,430 Average common stockholders' equity (GAAP) $ 1,018,277 $ 1,026,148 $ 1,010,318 $ 994,785 $ 991,977 $ 983,727 $ 435,635 Less: Average intangible assets 317,139 316,355 317,934 318,131 320,906 333,495 73,205 Average tangible common stockholders' equity (non - GAAP) $ 701,138 $ 709,793 $ 692,384 $ 676,654 $ 671,071 $ 650,232 $ 362,430 ROE (GAAP) 7.34% 7.02% 7.68% 7.79% 6.76% 5.30% 7.89% ROTCE (non - GAAP) 10.66% 10.15% 11.20% 11.45% 10.00% 8.02% 9.48% Common equity to total assets (GAAP) 11.56% 11.56% 11.71% 11.88% 12.94% 13.28% 10.48% Tangible common equity / tangible assets (non - GAAP) 8.32% 8.32% 8.36% 8.41% 9.20% 9.27% 8.93% 42

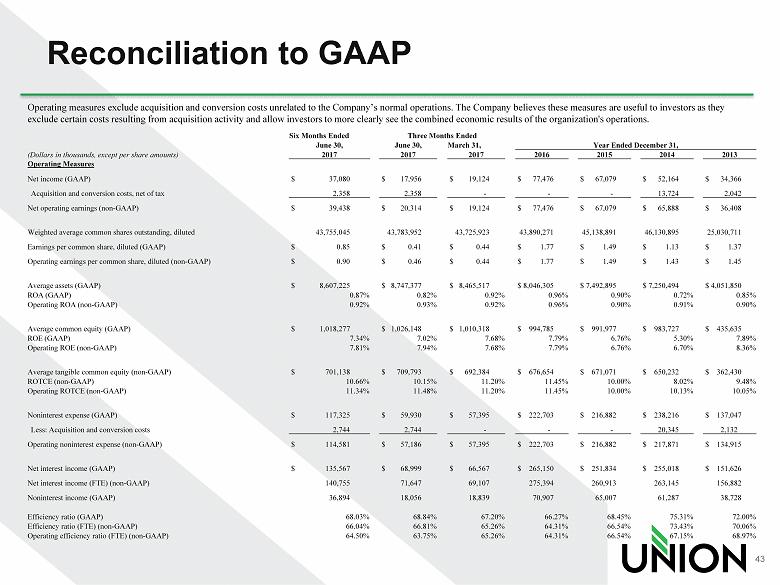

Operating measures exclude acquisition and conversion costs unrelated to the Company’s normal operations. The Company believe s t hese measures are useful to investors as they exclude certain costs resulting from acquisition activity and allow investors to more clearly see the combined economic resul ts of the organization's operations. Six Months Ended Three Months Ended June 30, June 30, March 31, Year Ended December 31, (Dollars in thousands, except per share amounts) 2017 2017 2017 2016 2015 2014 2013 Operating Measures Net income (GAAP) $ 37,080 $ 17,956 $ 19,124 $ 77,476 $ 67,079 $ 52,164 $ 34,366 Acquisition and conversion costs, net of tax 2,358 2,358 - - - 13,724 2,042 Net operating earnings (non - GAAP) $ 39,438 $ 20,314 $ 19,124 $ 77,476 $ 67,079 $ 65,888 $ 36,408 Weighted average common shares outstanding, diluted 43,755,045 43,783,952 43,725,923 43,890,271 45,138,891 46,130,895 25,030,711 Earnings per common share, diluted (GAAP) $ 0.85 $ 0.41 $ 0.44 $ 1.77 $ 1.49 $ 1.13 $ 1.37 Operating earnings per common share, diluted (non - GAAP) $ 0.90 $ 0.46 $ 0.44 $ 1.77 $ 1.49 $ 1.43 $ 1.45 Average assets (GAAP) $ 8,607,225 $ 8,747,377 $ 8,465,517 $ 8,046,305 $ 7,492,895 $ 7,250,494 $ 4,051,850 ROA (GAAP) 0.87% 0.82% 0.92% 0.96% 0.90% 0.72% 0.85% Operating ROA (non - GAAP) 0.92% 0.93% 0.92% 0.96% 0.90% 0.91% 0.90% Average common equity (GAAP) $ 1,018,277 $ 1,026,148 $ 1,010,318 $ 994,785 $ 991,977 $ 983,727 $ 435,635 ROE (GAAP) 7.34% 7.02% 7.68% 7.79% 6.76% 5.30% 7.89% Operating ROE (non - GAAP) 7.81% 7.94% 7.68% 7.79% 6.76% 6.70% 8.36% Average tangible common equity (non - GAAP) $ 701,138 $ 709,793 $ 692,384 $ 676,654 $ 671,071 $ 650,232 $ 362,430 ROTCE (non - GAAP) 10.66% 10.15% 11.20% 11.45% 10.00% 8.02% 9.48% Operating ROTCE (non - GAAP) 11.34% 11.48% 11.20% 11.45% 10.00% 10.13% 10.05% Noninterest expense (GAAP) $ 117,325 $ 59,930 $ 57,395 $ 222,703 $ 216,882 $ 238,216 $ 137,047 Less: Acquisition and conversion costs 2,744 2,744 - - - 20,345 2,132 Operating noninterest expense (non - GAAP) $ 114,581 $ 57,186 $ 57,395 $ 222,703 $ 216,882 $ 217,871 $ 134,915 Net interest income (GAAP) $ 135,567 $ 68,999 $ 66,567 $ 265,150 $ 251,834 $ 255,018 $ 151,626 Net interest income (FTE) (non - GAAP) 140,755 71,647 69,107 275,394 260,913 263,145 156,882 Noninterest income (GAAP) 36,894 18,056 18,839 70,907 65,007 61,287 38,728 Efficiency ratio (GAAP) 68.03% 68.84% 67.20% 66.27% 68.45% 75.31% 72.00% Efficiency ratio (FTE) (non - GAAP) 66.04% 66.81% 65.26% 64.31% 66.54% 73.43% 70.06% Operating efficiency ratio (FTE) (non - GAAP) 64.50% 63.75% 65.26% 64.31% 66.54% 67.15% 68.97% Reconciliation to GAAP 43